Working for yourself can be quite a rewarding achievement, but it’s also a lot of hard work, not to mention the amount of time it takes to learn how to properly claim your taxes. As an entrepreneur myself, one thing I’ve always had trouble understanding was exactly how one can claim their fixed assets, like a new car, laptop or cell phone.

So, in order to get the answers I needed and to help all of you out in the process, I asked Christian Schmidt, Founder, Tax Advisor, and Lawyer at Rechts- und Steuerberatung Schmidt in Düsseldorf, to put together this post for us!

As an entrepreneur, you record your assets, earnings, and expenses in your accounting and in your annual cash-method of accounting (“Einnahmen-Überschussrechnung” short “EÜR”) or balance sheet. However, certain expenses have a special character and will be treated separately. A special form of expenditure is fixed assets.

How to define fixed assets

Fixed assets represent assets that are intended to serve the company on a permanent basis. Fixed assets cannot only be physical objects, but also rights or financial assets. The only condition is that the material or immaterial object remains in the company for a longer period of time and is used there.

Example: For your business activity, you buy a multifunction printer for 900.00 € and copy paper for 50.00 €. The printer is an item you are likely to use for a long time in your business. It is, therefore, a fixed asset that is given special consideration in your bookkeeping. The copy paper is a common office supply that is expected to be consumed within the near future and will not be allocated to the company in the longer term.

Fixed assets in your accounting

Costs for items to be categorized as fixed assets cannot simply be fully considered in your accounting in the year of purchase.

Basic case: The acquisition costs of an item must be distributed over a certain period of time. This means that each year only a part of the costs may be taken into account to reduce your profit. This process is called linear depreciation (“lineare Abschreibung”) of fixed assets. There are also other depreciation methods that will not be discussed here.

Note: It is different with the input VAT. If you, as an entrepreneur, are entitled to deduct input VAT, you may claim the input VAT in full at the time of purchase of the item.

Acquisition costs

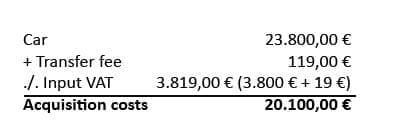

The acquisition costs of an item are basically the purchase price minus the input VAT (if you are entitled to deduct input VAT).

Example: You buy a car in August 2018 for 23.800,00 € gross. At the time of purchase, the dealer also charges a transfer fee of 119.00 € gross.

Subsequent acquisition costs

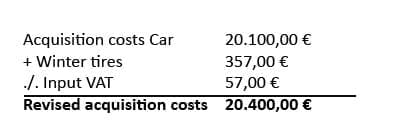

Acquisition costs may also include costs that were not incurred directly at the time of purchase (so-called subsequent acquisition costs). These are subsequently added to the acquisition costs.

Example: In December 2018, you will buy a set of winter tires for your vehicle for 357.00 € gross, which was previously only equipped with summer tires.

Calculation:

Average useful life – How long do the assets serve the company?

The useful life indicates how long the item is expected to serve the company before it is worthless. An asset becomes worthless in that it deteriorates due to its aging or becomes completely unusable and thus is unlikely to obtain a sales price on the market.

The useful life is usually calculated according to the depreciation table (“Afa-Tabelle”) officially published by the tax authorities. This table determines the usual useful life for objects of any kind. In justified cases, however, this can be deviated from.

Example: In January 2018 you buy a desk for 1,190.00 € gross. The useful life for office furniture is 13 years, according to the depreciation table. The input VAT amount of € 190.00 is fully deductible in the month of January 2018. The acquisition costs will be depreciated over a period of 13 years.

1.000 € / 13 years useful life = annual amount of 76,92 €.

Your profit will be reduced over the next 13 years by 76.92 € annually.

Depreciation table (“Afa-Tabellen”)

On Lexoffice, you can find a good overview of the depreciation period of generally usable assets (only in the German language):

Industry-specific depreciation tables can be found on the website of the Federal Ministry of Finance.

Directory of fixed assets

For fixed assets, a separate directory must be maintained (“Anlagenverzeichnis”). There, the item is listed with:

- its acquisition date,

- the acquisition cost,

- the depreciation amounts and

- the corresponding residual book value at the end of the year.

Normally, your respective software creates this directory directly from the bookkeeping.

A special form of fixed assets: Low-value assets

Low-value assets are subject to special rules for the determination of your profit. The requirements are as follows:

- The object is independently usable

- The acquisition costs for the object do not exceed the corresponding euro limits

What does it mean to use independently?

An item cannot be used independently if it can only be used in conjunction with other items.

Example: You buy a monitor for your PC for 80,00 € gross, an office lamp for 100,00 € gross, a roll container for 357,00 € gross and a desk for 963.90 € gross. The monitor works only in interaction with the PC. It thus does not meet the first requirement for a low-value asset. Consequently, the linear depreciation is applicable. The office lamp, the roll container, and the desk, however, can be used independently and fulfill this requirement.

The different euro limits

Assets between 0,01 € – 250,00 € net

For items that have a purchase price of € 0.01 – € 250.00 net, the following applies: The acquisition costs can be depreciated immediately and need not be depreciated over a certain period. In addition, items between € 0.01 and € 250.00 have the advantage that they do not have to be listed separately in your directory of assets.

Example: The useful life of the above-mentioned desk lamp would be 12 years. However, since the acquisition costs are less than € 250.00 net, it can be booked as a low-value asset. The costs are fully taken into account in the year of acquisition and also reduces your profit in the year of purchase. Furthermore, the lamp does not have to be included in the directory of assets.

Assets between 250,01 – 800,00 € net

For items that meet this euro limit, the same applies as above. The acquisition costs can be taken into account directly in the year of purchase and also reduces the profit in the year of purchase. Depreciation over a certain period is not necessary.

The only difference: Objects of this type have to be included in a directory of assets.

Example: The roll container has a purchase price of € 300.00 net and is thus in the range between € 250.01 and € 800.00. Therefore, it can be completely deducted from the profit in the year of acquisition. However, the roll container, unlike the desk lamp, must be included in the directory of assets.

Assets between 250,01 – 1.000,00 € net – Pool depreciation

Another special feature in the choice of depreciation methods is the so-called pool depreciation.

It allows assets that actually exceed the limit of € 800.00 net and thus no longer are covered by the lower-value assets to be depreciated over a shorter useful life than intended. All assets whose acquisition costs are between € 250.01 and € 1,000.00 are summed up into a so-called pool. The resulting value of this pool is then depreciated over a useful life of five years. This is particularly advantageous for items whose useful life actually exceeds five years.

Example: The desk mentioned above basically has a useful life of 12 years. With the acquisition cost of € 810.00 net, this would result in an annual depreciation amount of € 67.50 (€ 810/12 years). However, if the pool depreciation is applied to the desk, the depreciation is € 162.00 (€ 810/5 years) per year.

Note: If you decide to apply the pool deduction in one year, you will need to apply it for all items purchased during the year between € 250.01 and € 1,000.00. This might be disadvantageous.

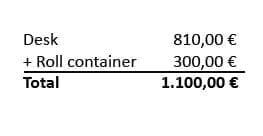

Example: If you decide to include the desk in the pool and depreciate it over a period of five years, you must also apply this rule to the roll container – which could have been immediately depreciated – because the acquisition cost of the roll container is also between 250.01 € and € 1,000.00 €.

The value of the pool is € 1,110.00 and will be depreciated over five years.

Recommendation: You can decide at the end of each year whether forming a pool is more favorable than depreciating the items individually. It is advisable to calculate the different options to choose the most favorable method.

Have any additional questions related to taxes and claiming work expenses? Contact Christian Schmidt and his team at Rechts- und Steuerberatung Schmidt.

Have more questions about taxes in Germany? So did others! Check out all the Life in Düsseldorf posts on Taxes!