If you plan on staying in Düsseldorf for the long run, perhaps you might be considering purchasing a property while the interest rate in the German real estate market remains historically low. Many people choose this option as it saves you from paying rent down the road. Given that buying a home is likely the biggest purchase you’ll ever make in your life, getting a mortgage can be quite an intimidating experience for expats, especially in a country where you’re unfamiliar with the process. However, if done properly with guidance, it can be a great way to help build wealth over time. I’ve just made the big house-buying leap too!

This is why I’ve partnered up with LoanLink, a mortgage broker specialized in helping expats in Germany get a home loan, to share with you the 5 most important tips you need when planning to apply for home financing.

This blog post was paid for by LoanLink. We take the quality of our website very seriously and only ensure the best content is published, regardless of sponsored or non-sponsored content. We trust and love all the brands we work with, enough to recommend them to you, our loyal readers!

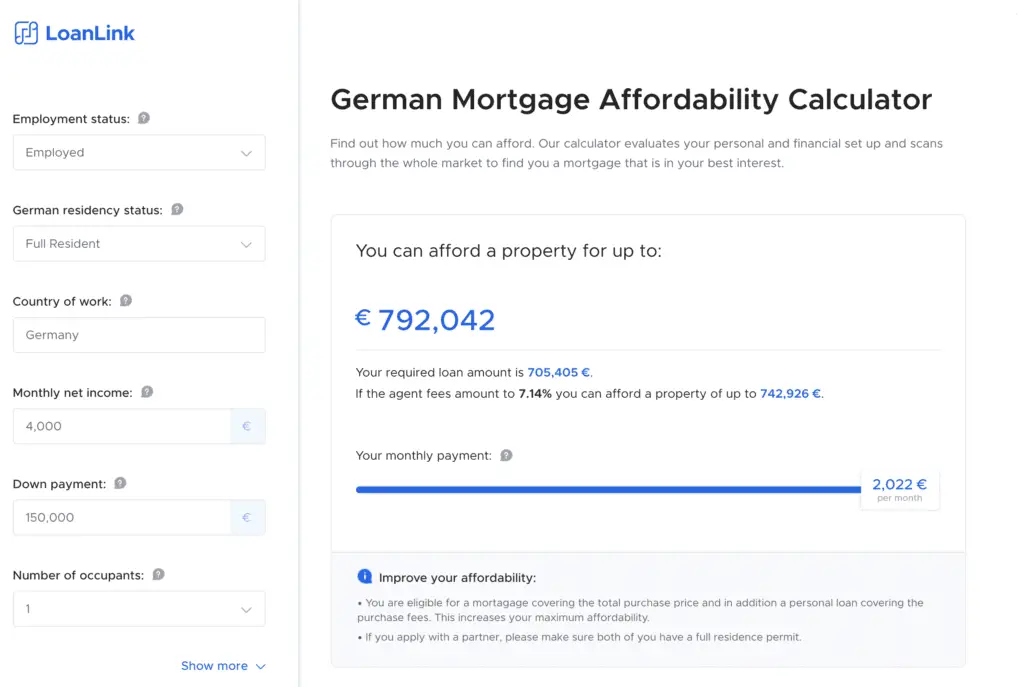

Find out what you can really afford

Even though looking for your dream home is very exciting, it’s essential to see if you are eligible for financing and to know what type/size of house you can truly afford so you don’t end up only finding properties that are out of your price range.

You can quickly get an accurate idea of how much you can afford and borrow by playing around with a mortgage affordability calculator for German home buyers. All you have to do is to answer a few questions, including down payment, net income, your residency status, and property location, then you will get an answer on the range of the property you can afford, and instantly. The calculator also offers advice on how to increase your borrowing capacity.

It’s definitely worth spending some time playing around with this mortgage affordability calculator (it’s completely free), as this can help you understand how much you can afford and how much down payment you’d need, so you can set a goal amount. This way you can ensure that you’ll be able to buy your dream home comfortably without sacrificing your financial future.

Getting a mortgage pre-approval

Getting a mortgage pre-approval helps you learn whether you are qualified for home financing. What’s more, the process reveals how much of a loan you could expect to receive from the lender based on your income, debt, and assets. Being pre-approved helps you show sellers that you qualify for a loan, and is an important first step.

Today’s property markets are competitive, especially in Düsseldorf. Sellers strongly prefer buyers with pre-approval. Some sellers even refuse to enter into negotiations until the buyer can prove that they qualify for a home loan. To make sure you have the best chance of securing a home, it’s best you get a mortgage pre-approval before you start house hunting.

The process of getting pre-approved is straightforward. You’ll have to complete an application and provide the lender with some documents. With LoanLink, once you’ve submitted a few required documents online if approved, you will receive a loan pre-approval certificate within 24 hours.

Understand what affects your interest rate

Although it’s up to the banks to decide the interest rate charged on your mortgage, understanding the factors that affect your mortgage interest rate can help you better prepare for when you negotiate your interest rate with the lender. There are two groups of factors on which you can have influence: financing and your personal circumstances.

When banks decide on the mortgage interest rate, the decision usually hinges on whether borrowers can repay the loan and how fast they’d be able to pay it off. Thus, in order to assure your lender that you have the capability to repay the mortgage and offer you a favorable interest rate, it’s vital to offer a hefty down payment and collateral. The more you put down, the lower your mortgage interest rate could be, as this helps prove your creditworthiness and also gives you more equity in the property.

Another important factor that affects your interest rate is your credit score (Schufa). As mentioned earlier, the interest rate lender charge on your mortgage is determined by how likely you’ll be able to pay off the mortgage entirely. Naturally, those with higher credit scores are oftentimes eligible for lower interest rates since they’ve proven themselves to be trustworthy borrowers in the past. If you’re new to Germany and don’t have a Schufa score yet; don’t worry, since no record simply means you have no bad credit history.

Take advantage of state funding programs

In Germany, many home builders and buyers can benefit through various low-interest-rate programs launched by the German government-owned development bank – Kreditanstalt für Wiederaufbau (KfW). They have different programs that aim to help people mortgage, build, or renovate a home. Borrowers can often combine one funding program with others.

For example, most homeowners are likely to be qualified for the KfW Residential Property Program 124. This program promotes the purchase or construction of owner-occupied homes or apartments. You can borrow up to €50,000 at a discount interest rate that is usually lower than what most mortgage lenders offer. You can use the fund to cover land acquisition, construction costs, and ancillary costs or purchase cooperative shares to obtain membership in a housing cooperative.

KfW also promotes home renovation projects that enhance energy efficiency. You can borrow at a discount interest rate and receive a subsidy of up to €27,500 to help repay the loan. And if your home is refurbished as a “KfW Efficient House”, you can apply for a grant up to €100,000. KfW allows borrowers to repay the loan completely or with installments of €1,000 or more.

Choosing an Independent Mortgage Broker

Finding the right mortgage can be overwhelming and strenuous. This is why it’s common for many people to go straight to their bank to find a mortgage rather than shopping around. However given that there are over 400 mortgage lenders in the German real estate market and each bank has different criteria when assessing mortgage interest rates, you may not be able to find the most favorable rate by just going to a bank directly. And since mortgage interest rates and fees can vary greatly from lender to lender, even small differences in the interest rate or administrative fees can incur a great amount of extra payment over the course of a loan.

Therefore, you should consider using an online comparison website to compare competitive pricing based on how much you need and how long you intend to pay it back. You should also consider hiring an independent mortgage broker who can help you find the right deals by comparing different mortgage offers for you. This would save you a significant amount of time for an already stressful process. Compared to a traditional mortgage broker where you have to get an appointment well in advance, working with a digital mortgage broker is much less complicated and stressful. You can also fill out the online mortgage application anywhere, anytime.

Another major advantage of using a digital mortgage broker is it eliminates any potential human errors. Humans can overlook crucial details that prevent you from getting the mortgage deal that best suits each customer’s unique profile and objectives. But with digital mortgage brokers, since they rely on an advanced, bias-free algorithm to find mortgages, their advice is always backed by data and is highly transparent. Hence, they are held fully accountable to help you choose the right mortgage.

Finally…

Working with a mortgage broker can ensure that you receive a tailor-made mortgage solution that suits your personal situation. Although you may think hiring a mortgage broker would add to the cost, some actually don’t charge a fee. For example, LoanLink won’t charge you a penny, as they only get paid by the lender after you’ve closed a mortgage.

Still, have questions? You can schedule a call with the mortgage experts at LoanLink by email service@loanlink.de or phone +49 (0) 30 5683 7535.